_page-0007(1).avif)

.avif)

.avif)

.avif)

Zero deposit home loans hit record highs

- More than 56% of all home loan applications now require no deposit, reflecting changing buyer affordability dynamics.

- Approval rates for 100% and cost-inclusive home loans have reached their highest levels in a decade.

- Banks are actively supporting housing demand by lowering barriers to entry for qualified buyers.

South Africa's home loan landscape is changing

South Africa's residential property market is witnessing a significant shift in home financing behaviour, with demand for zero-deposit and cost-inclusive home loans reaching record levels.

Latest data from ooba Home Loans reveals that more than 56% of all home loan applications submitted during the first four months of 2026 were for 100% home loans requiring no deposit from buyers.

This represents a two-percentage-point increase compared to the same period last year and signals a growing reliance on bank-funded property purchases.

The trend comes amid continued competition among South Africa's major banks, which are not only offering attractive discounts to the prime lending rate but are increasingly willing to provide higher loan-to-value financing to qualifying buyers.

According to Rhys Dyer, CEO of the ooba Group, the figures reflect both economic realities and a willingness by lenders to support homeownership.

"This data may underline the lack of available deposits among homebuyers, but it also shows the banks' willingness to enable and empower homebuyers in a tough economic climate."

He says many prospective buyers simply cannot afford to save for both a deposit and the additional costs associated with purchasing a property.

"For some, saving for a deposit and covering the associated transaction costs is no longer viable. However, they still have the affordability and income to repay their loan each month, and this is where these types of loans help reduce the barrier to entry."

Faster path to property ownership

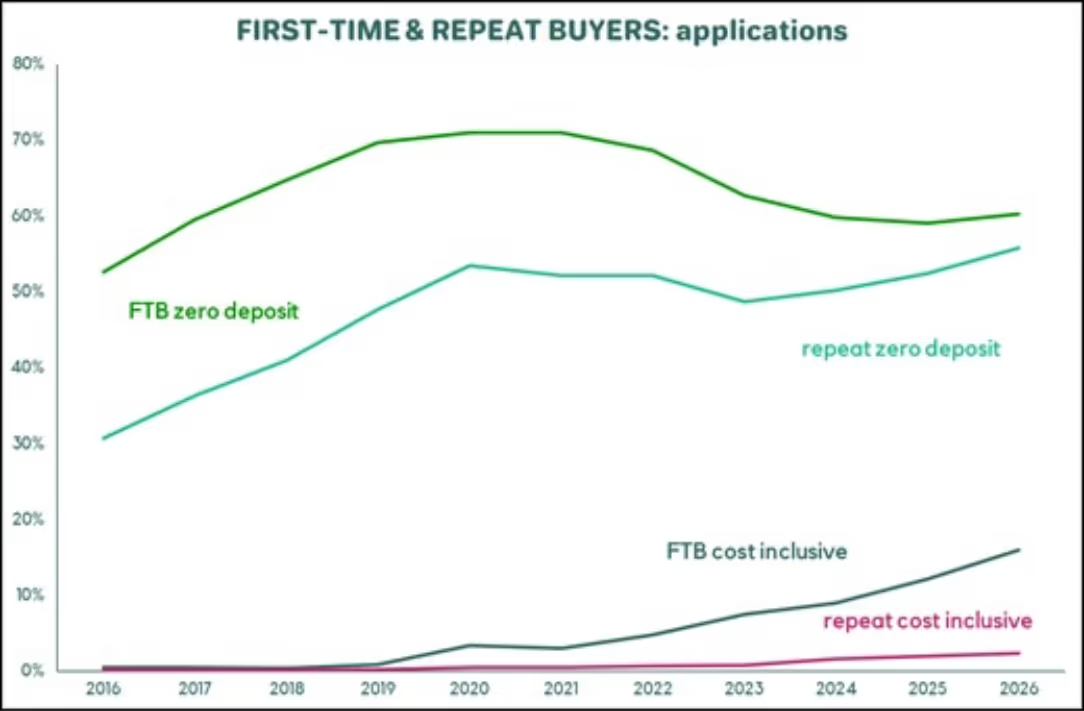

The strongest demand for zero-deposit financing is emerging from first-time homebuyers. Between January and April 2026, 60.2% of all first-time buyer home loan applications were for 100% home loans.

Demand for cost-inclusive home loans, which cover both the purchase price and transaction-related expenses, has risen even more dramatically.

Since 2021:

- Demand for 100% home loans among first-time buyers has remained consistently around 60%.

- Demand for cost-inclusive home loans has surged from just 3% of applications to nearly 16%.

The trend highlights the increasing challenge faced by younger buyers trying to accumulate the upfront capital traditionally required to enter the property market.

For many aspiring homeowners, access to cost-inclusive financing is becoming the difference between buying now and postponing homeownership indefinitely.

Banks are saying yes more often

Perhaps the most encouraging aspect of the data is that banks are not simply receiving more applications for these products, they are approving them at record rates.

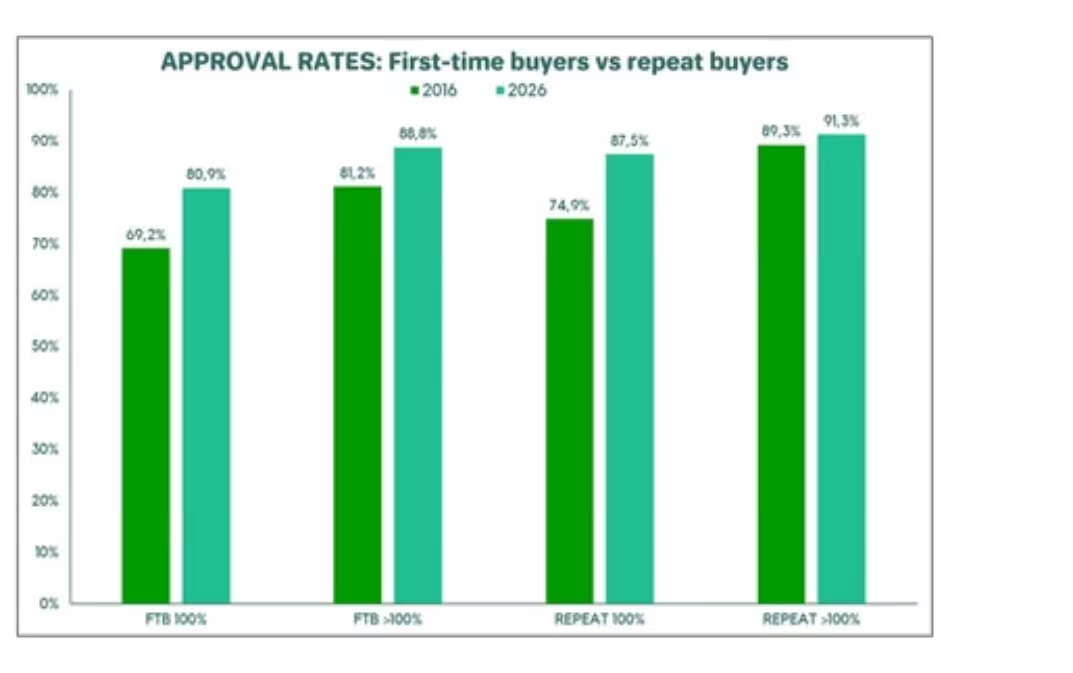

Approval rates for first-time buyers applying for 100% home loans have climbed steadily from 69.2% in 2016 to 80.9% in early 2026.

Cost-inclusive home loans have performed even better, with approval rates reaching an impressive 88.8%.

Banks are also supporting affordability through discounted bond registration costs and other incentives aimed at helping buyers enter the market. The value of homes financed through these products has also increased.

The average first-time buyer purchasing with a 100% home loan acquired a property valued at approximately R1.15 million, while buyers using cost-inclusive loans purchased homes averaging R994,297.

Repeat homebuyers seeking and getting 100% Finance

The trend is no longer limited to first-time buyers. Repeat homebuyers are increasingly turning to zero-deposit financing as traditional equity buffers come under pressure.

Applications for 100% home loans from repeat buyers have nearly doubled over the past decade and now account for 55.8% of all applications in this segment.

According to Dyer, slower house price growth in certain regions, particularly parts of Gauteng, has reduced the equity many homeowners would historically have relied upon to fund deposits when upgrading or relocating.

"Years of subdued house price growth have weakened the traditional equity buffer many repeat buyers previously enjoyed."

Cost-inclusive lending remains less common among repeat buyers, accounting for 2.3% of applications, as banks generally expect these buyers to cover their own transaction costs. Nevertheless, approval rates remain exceptionally strong.

From January to April 2026:

- Approval rates for repeat buyers applying for 100% home loans reached 87.5%.

- Cost-inclusive loan approvals climbed to 91.3%.

The average property purchased using a 100% home loan by repeat buyers was valued at R1.78 million, while cost-inclusive loan applicants purchased homes averaging R1.41 million.

Why are approval rates so high?

The willingness of banks to approve larger loans is not simply about stimulating demand. It is also underpinned by relatively healthy borrower performance.

Dyer says arrears levels among home loan applicants have remained contained, while household balance sheets in the middle-income segment continue to show resilience despite ongoing economic pressures.

He also credits stricter affordability assessments and robust prequalification processes.

"This positive trend is testament to the robust vetting and prequalification processes applied by companies like ooba Home Loans, ensuring that buyers are approved for an amount that is realistically aligned with what they can afford."

To qualify for 100% and cost-inclusive home loans, applicants generally require a credit score of 661 or higher, reinforcing the importance of responsible lending practices.

Banks continue supporting market recovery

Despite heightened geopolitical uncertainty, rising global energy prices and concerns around inflation, South Africa's banks have shown little indication of retreating from their supportive lending stance.

While lenders may become more cautious if international instability persists, the current environment remains favourable for qualified buyers.

The combination of competitive interest rate pricing, strong approval rates and increased access to 100% financing is helping sustain activity across the residential property market at a time when affordability remains a major concern.

Looking ahead

The rapid growth in zero-deposit and cost-inclusive home loans reflects a fundamental shift in the way South Africans are financing property purchases.

For first-time buyers, these products are accelerating access to homeownership. For repeat buyers, they are helping overcome weaker equity growth and affordability challenges.

Most importantly, they demonstrate a banking sector that remains committed to supporting housing demand and market recovery.

In an environment where saving a traditional deposit has become increasingly difficult, South Africa's lenders are playing a critical role in keeping the dream of homeownership within reach for thousands of qualified buyers.

.svg)

.avif)

.avif)