_page-0007(1).jpg)

.png)

.png)

.avif)

Homeowners aren’t as bond locked as they think

- Inland homeowners may have more built-up equity than they realise, making coastal moves more achievable.

- Bank competition and below-prime offers are helping strong buyers offset higher interest-rate pressure.

- Professional valuations, pre-qualification and accurate cost planning can turn “stuck” homeowners into active movers.

Home equity is changing the coastal relocation equation

Many South African homeowners who want to relocate to the coast believe they are trapped by higher interest rates, rising coastal prices and the fear that their current home equity will not stretch far enough.

But new market data suggests the reality may be more positive than many assume. According to Just Property, accumulated home equity, stronger bank competition and more informed financial planning are helping inland families unlock coastal moves even in a tougher interest-rate environment.

Recent FNB Property Barometer data shows national house price growth ranging between 3.4% and 3.7%, while the Western Cape continues to outperform many inland markets. This has reinforced the perception that families selling inland homes may struggle to afford comparable coastal properties.

For many homeowners, the maths feels intimidating. Entry-level homes in inland suburbs may start at around R1.2 million, while comparable coastal homes can begin closer to R1.8 million.

Paul Stevens, CEO of Just Property, says this is where the idea of being “bond-locked” has taken hold.

“When people talk about being ‘bond-locked’, they’re describing the feeling of being stuck. We’re seeing this among inland homeowners who want to move to the coast but believe that their current equity won’t cover coastal prices.”

He says the May interest-rate increase by the South African Reserve Bank, which raised the repo rate by 25 basis points to 7.00% and pushed prime to 10.50%, has added to affordability concerns.

But Stevens argues that many homeowners are not as trapped as they believe. “People are still moving. What has changed is the level of planning that’s needed because you can’t wing it in this market.”

He points out that 67% of estate agents surveyed by FNB expect market activity to increase, while BetterBond data shows banks are still competing for quality buyers, with some offering below-prime lending rates.

Seller misconceptions are holding people back

For Stevens, one of the biggest challenges is not affordability alone, but misinformation.

Many sellers underestimate how much equity they have built up over time. Others overestimate how much cash they need to move or assume that all coastal markets are beyond their reach.

Common misconceptions include:

- Believing the current home will not generate enough equity;

- Assuming coastal prices are unaffordable across the board;

- Delaying pre-qualification;

- Overestimating transfer and moving costs;

- Thinking they must sell before exploring their options.

Stevens says homeowners should start with facts, not fear. “First, get your property professionally valued. Once you know what your equity is, you’ll be able to make a decision based on fact, not fear.”

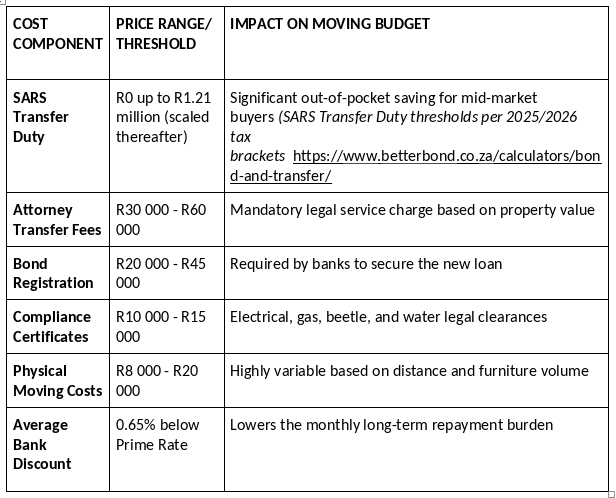

What it really costs to move

Before deciding that a move is impossible, sellers should complete a proper cost breakdown based on their own selling price, bond status and destination market.

For a mid-market transaction, the key cost components typically include:

Estimated moving cost components on a mid-market home purchase

Use a simple horizontal bar chart showing:

- Attorney Transfer Fees: R45,000 midpoint

- Bond Registration: R32,500 midpoint

- Compliance Certificates: R12,500 midpoint

- Physical Moving Costs: R14,000 midpoint

This will visually show readers that costs are real, but not always as prohibitive as feared.

More good news for 2016 - 2020 buyers

The outlook is especially encouraging for homeowners who bought between 2016 and 2020.

Many of these owners are sitting on meaningful equity gains, even if they have not calculated them recently. Stevens says industry records show the average purchase price for first-time buyers has risen to just under R1.2 million, while the national average home price has climbed to around R1.6 million.

That means a property bought for R1.2 million in 2018 may now be worth closer to R1.6 million, depending on location, condition and upgrades.

“People tend to underestimate how much equity they’ve built over time. When we show them the actual numbers, the conversation moves from ‘I can’t move’ to ‘I didn’t realise I had these options’.”

This is particularly relevant for sellers whose properties include sought-after features such as solar, battery backup, water resilience, security upgrades or energy-efficient improvements.

Younger buyers are increasingly prioritising homes with green, energy-resilient and safety features, which can improve saleability when properties are priced correctly.

Coastal dreams may require smarter choices

Stevens says sellers may need to broaden their thinking. A coastal move may still be achievable, but not always in the first-choice suburb or preferred property type.

Buyers should compare lifestyle value, proximity to schools, access to workplaces, monthly running costs and long-term affordability, rather than focusing only on square metreage or freehold ownership.

Sectional title homes may also provide a practical entry point into coastal markets.

“Sectional title units are generally the most affordable entry point in coastal areas, with lower maintenance and running costs,” says Stevens.

For families seeking a coastal lifestyle, the best opportunity may lie in suburbs offering similar lifestyle benefits but better brick-and-mortar value.

Feeling stuck is not the same as being stuck

The idea of being “bond-locked” is real for some households, particularly those under financial pressure or with limited equity.

But for many South African homeowners, the barrier may be more psychological than financial. With proper valuations, early pre-qualification, accurate cost planning and access to competitive lending, many inland families may find that a coastal move is more realistic than they thought.

As Stevens concludes: “Feeling bond-locked and being bond-locked are not the same thing. Once homeowners have the facts in front of them, many realise they’re far less stuck than they thought.”

For sellers, the lesson is clear: do the numbers before abandoning the dream. In today's market, equity, bank competition and better planning may be enough to turn a postponed coastal move into a practical next step.

.svg)

_page-0002.jpg)

_page-0006.jpg)

_page-0008(1).jpg)

.png)

.png)