_page-0007(1).avif)

.avif)

.avif)

.avif)

SA’s housing market is splitting in two

- Affordable housing demand is growing fastest, but formal bond finance remains severely constrained.

- Young buyers are entering the market later as affordability and credit pressures intensify.

- South Africa’s housing market is becoming increasingly divided between formal and informal financing systems.

Bond data exposes South Africa’s growing property divide

South Africa’s residential property market is undergoing a profound structural shift, one that is quietly reshaping the future of homeownership, wealth creation and housing finance in the country.

New data from Lightstone reveals a market becoming older, more expensive and increasingly polarised between a relatively resilient middle-to-upper income segment and a financially constrained affordable housing sector struggling to access formal mortgage finance.

The findings suggest South Africa’s housing challenges are no longer simply cyclical reactions to interest rates or economic slowdowns. Instead, they point to a deeper structural divide emerging within the country’s residential property ecosystem.

According to Hayley Ivins-Downes, Managing Executive Real Estate at Lightstone, South Africa now effectively operates within two parallel housing finance systems.

One is a formal, mortgage-led banking environment servicing primarily middle- and upper-income buyers. The other is a semi-formal or informal housing economy within the affordable sector, where access to traditional bank finance remains limited and property transactions are increasingly driven by cash purchases, family support structures and informal lending arrangements.

This divide matters enormously because the affordable housing segment represents the largest and fastest-growing portion of the market.

With more than 60% of South Africa’s estimated 63 million population under the age of 35, the affordable housing market effectively represents the gateway to future homeownership, wealth accumulation and long-term financial stability.

Yet the data suggests that gateway is narrowing.

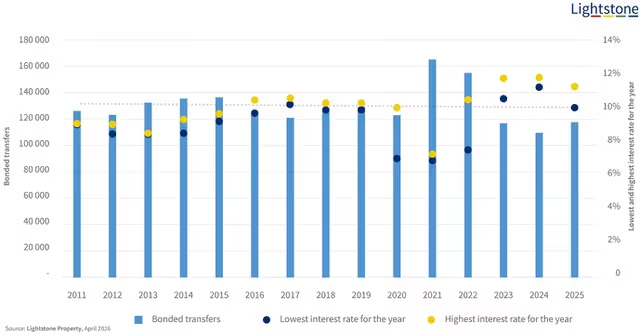

Bond Market Overview: Growth without real expansion

The data confirms the traditional relationship between interest rates and bond activity: as rates decline, mortgage activity generally improves.

However, the broader picture is more concerning. Despite population growth and rising housing demand, the total number of bonded transfers has remained largely flat for more than a decade. The market recorded just 118,000 bonded transfers in 2025, only a modest recovery from the 15-year low of 110,000 recorded in 2024.

This suggests South Africa’s formal mortgage market is not expanding meaningfully in real terms. Instead, a growing portion of housing activity appears to be happening outside the traditional banking system.

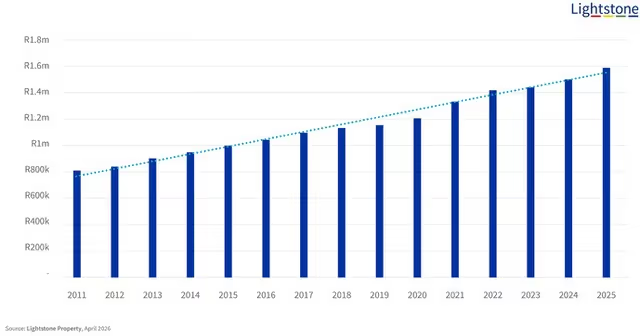

Property prices continue climbing

One of the clearest trends emerging from the data is the sharp rise in average bond values.

The average primary bond issued increased from roughly R800,000 in 2011 to approximately R1.6 million in 2025, effectively doubling over the period before inflation adjustments.

This reflects several structural realities:

- Higher property prices

- Escalating construction costs

- Municipal tariff increases

- Rising compliance and development costs

- Stronger performance in wealthier market segments

The result is a market increasingly inaccessible to first-time and lower-income buyers.

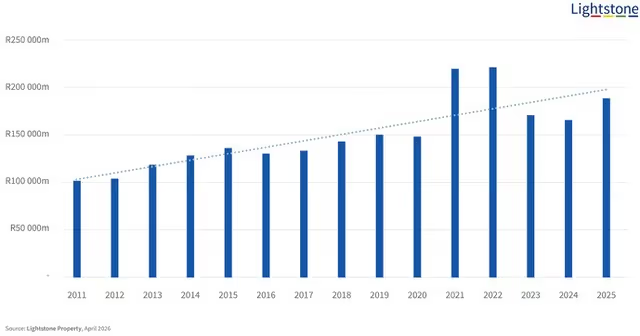

Total bond values reveal post-covid surge

While transaction volumes remained relatively subdued, the total value of bonds written surged significantly during the post-Covid period.

South Africa recorded a peak of R221.2 billion in total primary bond value during 2022 before moderating to R188.3 billion in 2025.

This highlights a critical trend:

Fewer properties are being financed, but at substantially higher values.

In practical terms, the formal mortgage market is becoming increasingly concentrated at the upper end of the market.

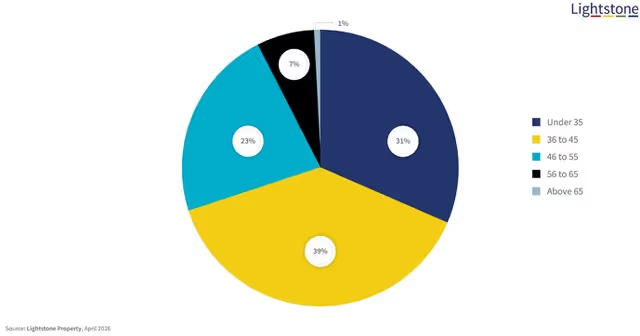

Younger buyers under pressure

Perhaps the most important long-term warning sign is the declining participation of younger buyers.

Buyers under the age of 35 accounted for just 31% of bond value in 2025, down sharply from approximately 40% before the Global Financial Crisis of 2008/9.

While younger buyers still participate in the market, they are increasingly entering later in life.

This delay has major long-term implications:

- Reduced lifetime wealth accumulation

- Delayed asset ownership

- Increased dependency on rental housing

- Lower intergenerational wealth transfer

- Greater financial vulnerability

The underlying drivers are well known:

- High unemployment

- Income instability

- Tightened credit scoring

- Elevated interest rates

- Rising living costs

- Deposit affordability challenges

The concern is that younger South Africans are not disengaging from homeownership by choice — they are increasingly being locked out structurally.

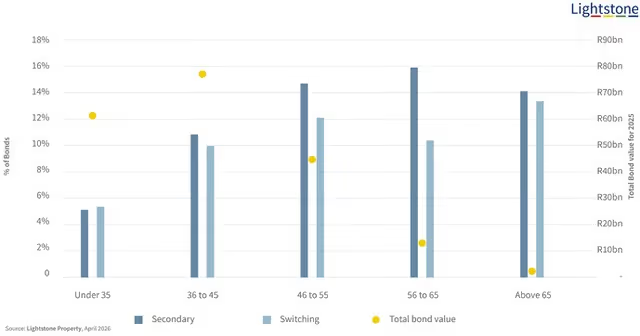

Older buyers dominate bond switching

The data also shows that older age groups dominate secondary bonds and bond switching activity.

Buyers aged 46 to over 65 account for the largest proportion of refinancing and secondary bond activity, while younger buyers remain least active.

This reinforces the widening wealth gap between established property owners and emerging buyers trying to enter the market for the first time.

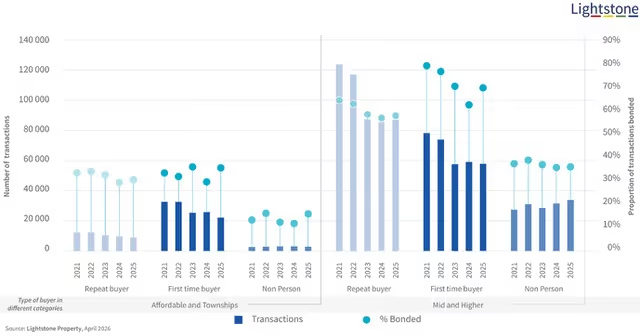

Affordable market faces financing squeeze

The affordable market presents the clearest evidence of South Africa’s housing finance divide.

Affordable first-time buyer transactions fell from 32,000 in 2021 to just 22,000 in 2025, a 32% decline. By comparison, middle-to-upper market first-time buyer transactions declined by 26% over the same period.

The difference is critical: The middle-to-upper market still retains relatively strong access to mortgage finance, while affordable buyers increasingly struggle to secure formal bank funding.

Affordable housing now relies heavily on:

- Cash transactions

- Informal lending

- Family financing

- Community-based support systems

- Delayed ownership patterns

Meanwhile, middle- and upper-income housing remains largely mortgage-driven and more integrated into the formal banking system.

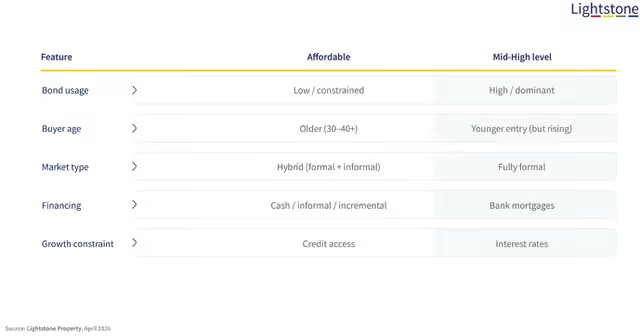

A structural divide is emerging

The data points to a property market gradually splitting into two very different realities.

Middle-Upper Market

- Stronger bond penetration

- Better access to formal credit

- Higher-value transactions

- Greater resilience to economic shocks

- Stronger wealth accumulation

Affordable Market

- Lower formal mortgage access

- Higher financial exclusion

- Greater dependence on informal financing

- Older first-time buyers

- Slower wealth creation

The long-term risk is that South Africa’s largest housing segment — affordable housing — becomes increasingly disconnected from the formal mortgage economy altogether.

Looking Ahead: What Needs to Change?

The findings raise serious questions for policymakers, banks and the broader property industry.

If affordable housing remains under-financed, South Africa risks:

- Slower mortgage market growth

- Entrenched inequality

- Lower homeownership levels

- Reduced economic mobility

- Weaker long-term household wealth creation

Several interventions could help reverse the trend:

- Faster title deed formalisation

- Alternative credit scoring recognising informal income

- Smaller and more flexible micro-mortgage products

- State-backed risk-sharing models with banks

- More serviced and bankable affordable housing developments

Without meaningful intervention, the country’s housing market could become increasingly fragmented between those with access to formal finance and those permanently excluded from it.

Summation

South Africa’s residential market is no longer simply reacting to interest rates or short-term economic cycles.

A deeper structural divide is emerging between a formal mortgage-driven market serving wealthier buyers and a constrained affordable sector battling limited credit access and rising financial exclusion.

The warning signs are already visible: fewer young bonded buyers, flat mortgage growth, rising property costs and growing dependence on informal financing structures.

The challenge now is whether South Africa can create a more inclusive housing finance system before this divide becomes permanently entrenched. Because ultimately, the health of the affordable housing market will determine the future health of the country’s entire property sector.

.svg)

_page-0002.avif)

_page-0006.avif)

_page-0008(1).avif)

.avif)

.avif)