_page-0007(1).avif)

.avif)

.avif)

.avif)

Pensioners power South Africa's property Market

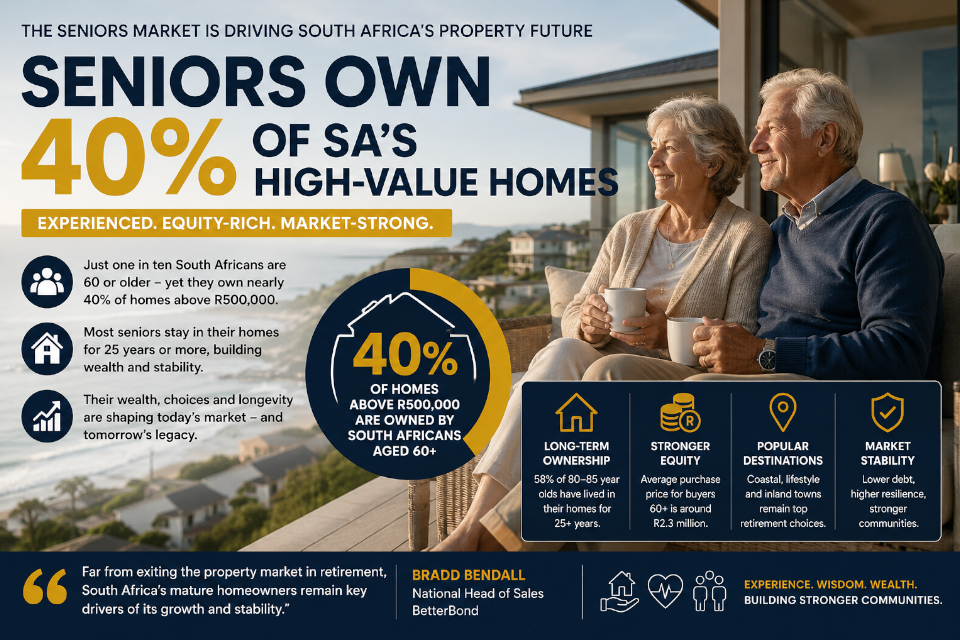

- South Africans over 60 own nearly 40% of residential property valued above R500,000.

- Retirees are staying in their homes longer, driving market stability and wealth preservation.

- Strong equity positions and limited debt make mature buyers a powerful property market force.

Retirees become a driving force in property

Contrary to the long-held belief that retirees downsize into smaller homes or retirement villages, South Africa's mature homeowners are emerging as one of the country's most influential property market segments.

While only around 10% of South Africans are aged 60 and older, this demographic controls almost 40% of the residential property market valued above R500,000, according to data from LOOM Property Insights.

Far from exiting the market, retirees are retaining high-value assets, purchasing lifestyle properties and contributing significantly to market stability.

"Far from exiting the property market in their retirement years, South Africa's mature homeowners remain key drivers of its growth and stability," says Bradd Bendall, National Head of Sales at BetterBond.

Many retirees have settled in coastal destinations, lifestyle estates and inland towns where they often account for a substantial share of local property ownership. In some areas, residents over 60 own as much as 60% of the housing stock.

The trend reflects changing retirement patterns, longer life expectancy, greater financial security and a desire to maintain established lifestyles rather than move into traditional retirement accommodation.

Supply and demand constraints reshape retirement living

One of the primary reasons retirees remain in conventional residential properties is the limited supply of retirement accommodation across the country.

According to LOOM Property Insights, for every one unit within a formal retirement development, there are approximately 30 properties owned by people aged 60 and older outside such developments.

South Africa currently has only around 650 formal retirement complexes, providing roughly 44,000 residential units. Demand for quality retirement accommodation continues to exceed available supply, with many developments reporting extensive waiting lists.

"The demand for well-located retirement developments often exceeds supply, and many retirees face long waiting lists," notes Bendall.

As a result, many older homeowners choose to age in place, remaining in familiar communities and adapting their existing homes to meet changing lifestyle requirements.

Longevity is changing housing behaviour

Longer life expectancy is also reshaping residential property ownership patterns.

Many mature homeowners entered the market decades ago when affordability was stronger, deposit requirements were lower and homeownership was more accessible. Over time, these owners have accumulated substantial equity while benefiting from decades of property value appreciation.

As a result, older homeowners are increasingly concentrated in the upper end of the residential market, particularly in properties valued above R2 million.

LOOM data reveals that 58% of homeowners aged between 80 and 85 have occupied their homes for more than 25 years. For owners older than 85, this rises to 65%.

These figures demonstrate a strong preference among retirees to remain in their homes for longer, reinforcing housing market stability while reducing turnover within established residential areas.

Mature buyers continue to spend

Retirement is no longer synonymous with reduced spending power.

BetterBond's data for the 12 months ending April 2026 shows that the average income of buyers aged over 60 increased by more than 8% year-on-year. During the same period, the average purchase price paid by these buyers rose by just over 8% to approximately R2.3 million.

Many retirees who choose to move are downsizing in size but not necessarily in value.

"Buyers who are moving out of their primary homes as their needs change may downsize but not downscale in value," says Bendall.

Years of capital growth have enabled many mature buyers to accumulate significant equity, allowing them to make large deposits or purchase properties with limited reliance on mortgage finance.

This strong financial position makes older buyers particularly attractive from a lending perspective and enables them to remain active participants in the property market despite broader economic uncertainty.

The latest FNB Estate Agents Survey further highlights the trend, with retirement accounting for 21% of all life-stage-related property sales.

Property choices are evolving

While retirement villages remain popular, the majority of older homeowners continue to favour traditional housing options.

LOOM data shows that among homeowners over 60 living outside retirement developments, approximately 80% reside in freehold homes, while only 20% live in sectional title schemes or residential estates.

This trend is creating new opportunities for developers and housing providers. As homeowners age, there is increasing demand for homes that incorporate universal design principles, including single-level living, wider walkways, walk-in showers, improved accessibility and integrated smart-home technology.

Developers are also seeing growing interest in inter-generational lifestyle estates that combine quality housing with healthcare services, recreational facilities and community amenities.

Geographically, retirees continue to favour lifestyle-driven locations, particularly along the West Coast, Garden Route and KwaZulu-Natal's North and South Coasts, where quality of life often outweighs proximity to major urban centres.

Economic stability anchors the market

Perhaps the most significant contribution of mature homeowners is the stability they bring to the residential property market.

Many own their properties outright or carry minimal debt, making them less vulnerable to interest rate fluctuations and economic volatility.

"As many mature homeowners own their properties outright or with minimal debt, they are largely insulated from interest rate fluctuations, which further supports housing market stability," says Bendall.

This financial resilience enables retirees to continue investing in property maintenance, municipal services, community security and local infrastructure, helping sustain neighbourhood values during periods of economic uncertainty.

At the same time, the concentration of wealth among older homeowners highlights a growing intergenerational asset divide. Younger buyers face increasing affordability challenges while older generations continue to hold a substantial share of higher-value residential assets.

Looking ahead

South Africa's retirees are no longer quietly exiting the housing market. Instead, they are emerging as one of its most influential and financially resilient segments.

With longer life expectancy, strong equity positions, rising spending power and limited retirement housing supply, mature homeowners are reshaping housing demand and strengthening market stability.

As billions of rands worth of residential property are eventually transferred to younger generations over the coming decades, the decisions made by today's retirees will continue to influence the country's property landscape well into the future.

.svg)

.avif)

.avif)