_page-0007(1).avif)

.avif)

.avif)

.avif)

Bond pain deepens after SARB’s surprise rate hike

- Homeowners now face hundreds of rands in extra monthly bond repayments following the first interest rate hike in three years.

- Property leaders warn affordability pressure is rising, but buyers should not abandon long-term property ownership goals.

- Rising fuel, food, electricity and municipal costs are forcing consumers to buy smaller, smarter and more strategically.

South African homeowners and property investors are now facing the real financial impact of the South African Reserve Bank’s latest 25 basis point interest rate increase, with monthly bond repayments climbing immediately across all price bands.

The increase pushes the prime lending rate to 10.5% and marks the first rate hike since May 2023, adding fresh pressure to an already strained consumer environment battling:

- rising fuel costs

- municipal tariff hikes

- electricity increases

- transport inflation

- and broader affordability pressure.

For many households, the increase may appear modest initially, but the additional monthly costs quickly escalate as property values rise.

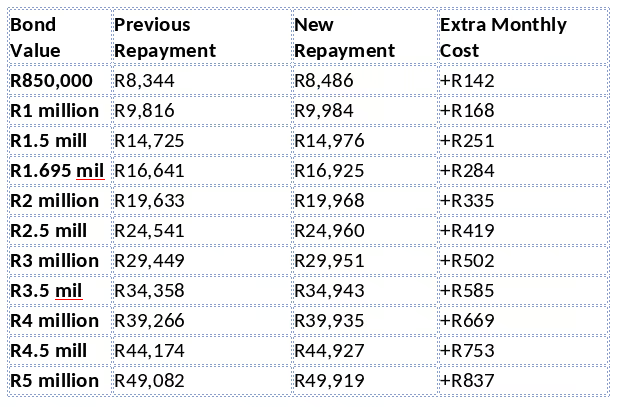

What the rate hike now costs you

A 25-basis-point increase translates into the following additional monthly bond repayments:

Based on the latest oobarometer figures, South Africa’s average home price now sits at R1,695,257, meaning the average homeowner will pay roughly R284 more every month following the hike.

While those numbers may not appear catastrophic individually, they arrive alongside escalating living costs across almost every category of household spending.

Berry Everitt: Buy smaller, buy smarter

Berry Everitt says the latest hike should serve as a wake-up call for buyers to prioritise affordability and financial resilience.

“The smartest buyers in this market are stress-testing their finances and asking themselves whether they could still comfortably afford the property if rates rise further and living costs continue climbing,” says Everitt.

He warns against borrowing at the absolute maximum banks are willing to lend and says buyers may need to adjust expectations by considering:

- smaller homes

- more affordable suburbs

- or entry-level properties.

However, Everitt cautions against delaying homeownership indefinitely while waiting for lower interest rates.

“Stock shortages are already emerging in parts of the market and prices could continue rising. In many cases, buying sensibly now still makes more financial sense than waiting,” he says.

Leapfrog: Buyers becoming more disciplined

Fritz Swanepoel says the increase places further pressure on already stretched household budgets, particularly among first-time buyers and highly leveraged consumers.

However, he believes the market has already spent years adapting to elevated borrowing costs. “Both buyers and sellers have become increasingly pragmatic and financially disciplined in how they approach property decisions,” says Swanepoel.

He notes that demand for quality, correctly priced property remains resilient, especially in areas offering:

- strong infrastructure

- lifestyle appeal

- security

- and economic opportunity.

Swanepoel also says semigration trends are becoming more balanced, with Gauteng regaining momentum as rising coastal living costs and return-to-office trends reshape buyer behaviour.

Rawson: The market is adapting

Tony Clarke says property remains fundamentally sensitive to interest rates, affordability and broader economic conditions.

“Property is fundamentally a credit-driven asset class. Interest rates, affordability, consumer confidence and broader economic conditions directly influence transaction activity and pricing dynamics,” says Clarke.

Craig Mott says while the increase adds pressure, it does not fundamentally change the market overnight.

“Buyers and homeowners have already spent the last few years adapting to changing conditions, and that resilience continues to show,” says Mott.

He believes buyers are increasingly focusing on:

- affordability

- long-term ownership value

- lifestyle convenience

- and operating costs

rather than speculative market timing.

FIRZT Realty: Don’t abandon your property goals

Stephen Whitcombe says buyers should avoid abandoning long-term property ownership plans because of the latest increase.

Instead, Whitcombe says the current environment makes professional mortgage advice and affordability planning even more important.

“A good mortgage originator can negotiate aggressively with multiple banks and often secure more favourable lending terms that can save buyers substantial amounts over the life of the loan,” he says.

Whitcombe also encourages existing homeowners to renegotiate rates with banks where possible, particularly clients with strong repayment histories.

Importantly, he believes Johannesburg still offers some of South Africa’s strongest relative property value, particularly for younger buyers entering the market.

“Property remains one of the most effective long-term wealth creation tools available to ordinary South Africans,” says Whitcombe.

The real property pressure is bigger than rates alone

The reality is that the latest rate increase is only one piece of a much bigger affordability problem facing South African households.

Consumers are simultaneously battling:

- rising petrol prices

- electricity hikes

- municipal increases

- food inflation

- transport costs

- and stagnant income growth.

That combination is forcing buyers, investors and homeowners to become:

- more disciplined

- more strategic

- and more financially cautious.

At the same time, however, property leaders remain broadly aligned on one important point: well-priced property in strong locations continues attracting demand.

The new era of smarter buying

The era of easy affordability is fading again. The market is increasingly rewarding:

- financially prepared buyers

- conservative borrowing

- realistic pricing

- strong locations

- and long-term thinking.

For many South Africans, the latest hike may delay decisions slightly.

But for disciplined buyers and investors, property still remains one of the country’s strongest long-term wealth-building assets.

The message from the industry is increasingly clear: buy smaller if necessary, buy smarter, but don’t stop building equity.

.svg)

_page-0002.avif)

_page-0006.avif)

_page-0008(1).avif)

.avif)

.avif)