_page-0007(1).avif)

.avif)

.avif)

.avif)

Smart Home Financing: Refinance or Personal Loan?

Top Takeaways

- Personal loans are quick and easy - ideal for small projects with fast turnaround needs and no collateral requirements.

- Refinancing taps into home equity - better suited for larger upgrades with lower interest rates over the long term.

- Readvancing offers hybrid flexibility - fast, affordable access if you’ve paid extra into your bond account

How to fund renovations without hurting your long-term wealth

Best Option Forward for Property Owners & Investors. The best funding route depends on your equity, urgency, and project size:

Use a Personal Loan if

- You need quick access to cash

- The project is relatively small

- You want to avoid bond changes or legal fees

Use a Readvance if

- You’ve paid extra into your bond

- You want quick access at home loan rates

- You’re doing mid-sized upgrades with minimal red tape

Use a Further Loan/Refinance if

- You’re planning major structural work or adding long-term value

- You have strong equity and a healthy credit profile

- You’re comfortable with extending your bond term for a lower rate

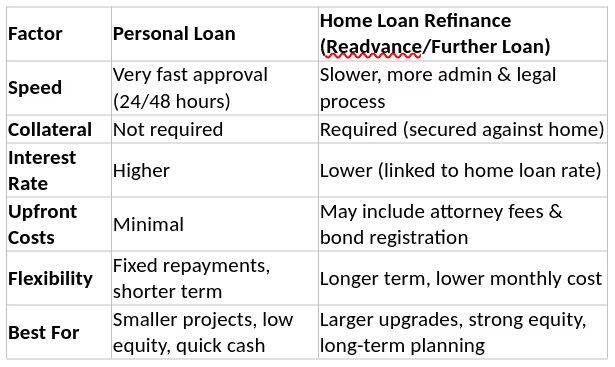

Refinance vs Personal Loan – The Pros & Cons

Summation

When renovating, it’s not just about how much you borrow, it’s about how smartly you borrow. Match your funding method to the scale of your renovation and your financial horizon. Always weigh short-term convenience against long-term equity and cost.

Wendy Beaumont is an Executive for Unsecured Lending at Nedbank

Share

.svg)

.avif)

.avif)